HCM Insights

Full Year 2022

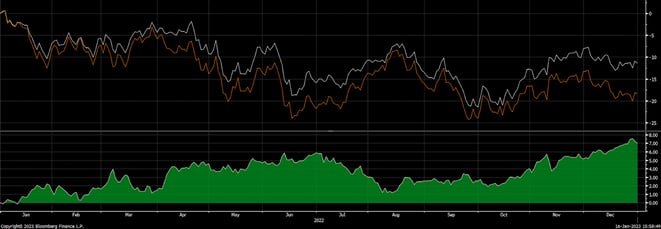

SMCO vs. Russell 2500

Absolute Performance (top panel) & Relative Performance (bottom panel)

2022 was a difficult year for equity investors, and the SMID (small- and mid-) cap space was not spared. A confluence of factors – led by aggressive Fed actions – soured the mood for risk assets. Interest rates more than doubled over the year, and as rates went up, so did economic concerns. Simultaneously, much of the Covid-spurred government largesse burned off, and the once powerful V-shaped economic recovery started to falter. All this impacted equity markets, and previously high-flying sectors saw 30% to 50%-level price declines not seen since the dot-com implosion.

We never view losing money as positive, but our ability to limit the downside for SMCO investors was encouraging. For the full year, the Russell 2500 was down 18.4%, while SMCO was down 11.2% (gross)/11.9% (net). Our focus is on the long term, and we firmly believe limiting drawdowns is an important aspect of creating attractive, long-term results.

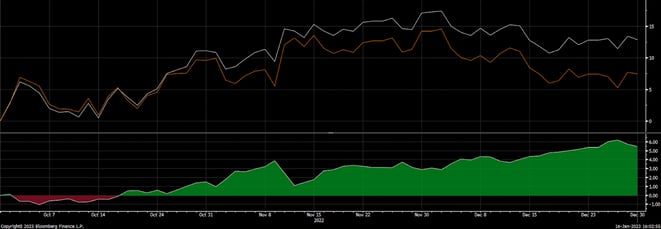

The fourth quarter offered a positive data point in an otherwise bleak year, with SMCO finishing on a solid note. SMCO returned 12.9% (gross)/12.7% (net), far outpacing the Russell 2500’s +7.4%. Q4 started with another strong positive market move, similar to last summer’s rally. Unlike the summer, SMCO kept pace this time, and as the market began to wobble again toward year-end, SMCO held a large portion of its gains. As portfolio companies reported solid Q3 results, during Q4, the market rewarded their shares.

4th Quarter Year 2022

SMCO vs. Russell 2500

Absolute Performance (top panel) & Relative Performance (bottom panel)

We are fundamental investors, focused on stocks where we see an improving fundamental picture coupled with an attractive valuation. For several years we have been operating in a world of near-zero interest rates and seemingly unlimited liquidity. In our opinion, this has led to less investor scrutiny of business characteristics necessary to sustain long-term success. As such, fundamentals have taken a backseat, and for stretches of time, valuation has been seen as a “so what” factor. Conditions have now changed.

Interest rates may move up and down, but we believe a return to a zero-rate world seems unlikely. Additionally, with returns available in more asset classes, the need to take excess risk and the desire to pursue speculation in search of return have ebbed. These changes have profound impacts on equity investing but, importantly, could also have real-world consequences that would reinforce the value of good businesses in a circular fashion.

What if less well-run enterprises cannot rely on perpetual, near-free financing? The better operators will be the ones attracting capital, not the faster-growing but less well-managed challengers. Over time this likely bolsters the market share and returns of the better companies. Recently we have caught glimpses of the market “caring more” about results – not just growth but also margins and returns. Could we be headed toward a more rational market, where the ability to grow must be balanced against the ability to fund that growth? Perhaps. We have been able to perform even when the market was less discriminating: We’d love to invest in a market where investors hold companies to task.

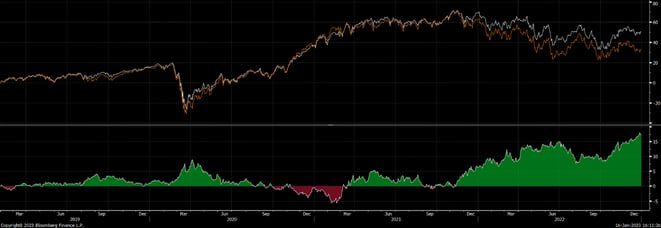

Lastly, long-term risk-adjusted results are what we value most. The SMID-cap portion of the stock market is inherently risky but, in our opinion, also full of opportunity. We aim to deliver an attractive, over-the-cycle return for our investors. We have been managing SMID strategies for 25 years and now have nearly four years of a live track record at Hilton. Since SMCO’s launch, we have experienced bull markets, bear markets, a once-in-a-century pandemic, a level of financial accommodation never before tried, and now the withdrawal of that support. We think it is fair to say that while four years (three years and eleven months, to be exact!) may not be a long time in calendar terms, the last four years equates to a lot more in dog years.

We view a calendar turn as somewhat of an arbitrary point in time. That said, it is a good time to reflect, not only on the last year but on the last few years. In that vein, we are encouraged that SMCO has generated an annualized return of 10.9% (gross)/10.2% (net) versus an annualized gain of 7.5% for the Russell 2500 over the same time. Protecting investor assets in a bear market is great, but the market is up more often than it is down. A successful strategy must also participate in uptakes, and we would submit that our record shows that we can.

We look forward to managing SMCO in this fashion for years to come. We are process driven and draw on a wealth of experience. As always, we remain vigilant.

Inception to Date (2/1/2019 – 12/31/22)

SMCO vs. Russell 2500

Absolute Performance (top panel) & Relative Performance (bottom panel)

Please see the Small & MidCap Opportunities Factsheet which contains full performance information as well as relevant legal and regulatory disclaimers.