HCM Insights

The long-standing positive correlation between equity prices and Treasury bond yields has reversed course in recent years. Since 2022, we've observed more frequent intervals of negative correlation, interrupting the positive correlation pattern of the past decade.

When stock prices and bond yields move together (positive correlation), an investment strategy incorporating diversification helps spread risk across different asset classes, with bonds offering protection when equities face volatility.

During periods of negative correlation, when stock prices decline and Treasury yields increase (pushing Treasury prices lower), the absence of a natural hedge exposes portfolios to greater risk and decline, causing significant pain for investors.

Let's take a closer look at these recent shifts, the role of inflation and interest rates, and how these elements can affect asset performance.

Price Correlation Drivers

Broadly speaking, several factors can influence the direction of correlations, including economic growth expectations, inflation, interest rates, and market supply and demand dynamics. Here are a few to consider:

Positive Price Correlation

A positive correlation between equity prices and Treasury yields often reflects strong investor sentiment about the direction of economic growth. The "risk on" trade typically sees stock prices and Treasury yields rise in tandem as anticipated economic growth drives investors toward equities and away from bonds.

Conversely, the "risk off" trade occurs when economic uncertainty increases, causing equity prices and Treasury yields to fall simultaneously as investors seek the safety of bonds.

As mentioned, this environment is especially advantageous for multi-asset solutions, enabling bonds to serve as a buffer against equity instability.

Negative Price Correlation

Rising inflation expectations typically drive Treasury yields up as investors demand higher returns to offset purchasing power erosion. This often coincides with anticipated Fed rate hikes, further driving yields up as bond prices fall in response to tighter monetary policy.

Simultaneously, equity prices often face downward pressure due to squeezed profit margins and increased borrowing costs. This dynamic results in an inverse relationship between rising bond yields (declining bond prices) and falling equity prices一and an often punishing investment environment.

That said, rising inflation can sometimes complicate the equity-bond correlation. Companies with strong pricing power can maintain profit margins by passing costs to consumers, while sectors such as finance may benefit from higher interest rates, potentially dampening downward pressure on equity prices.

Correlation Reversals: 2021-24

While it’s challenging to pinpoint the exact causes of recent negative reversals, inflation likely played a significant role.

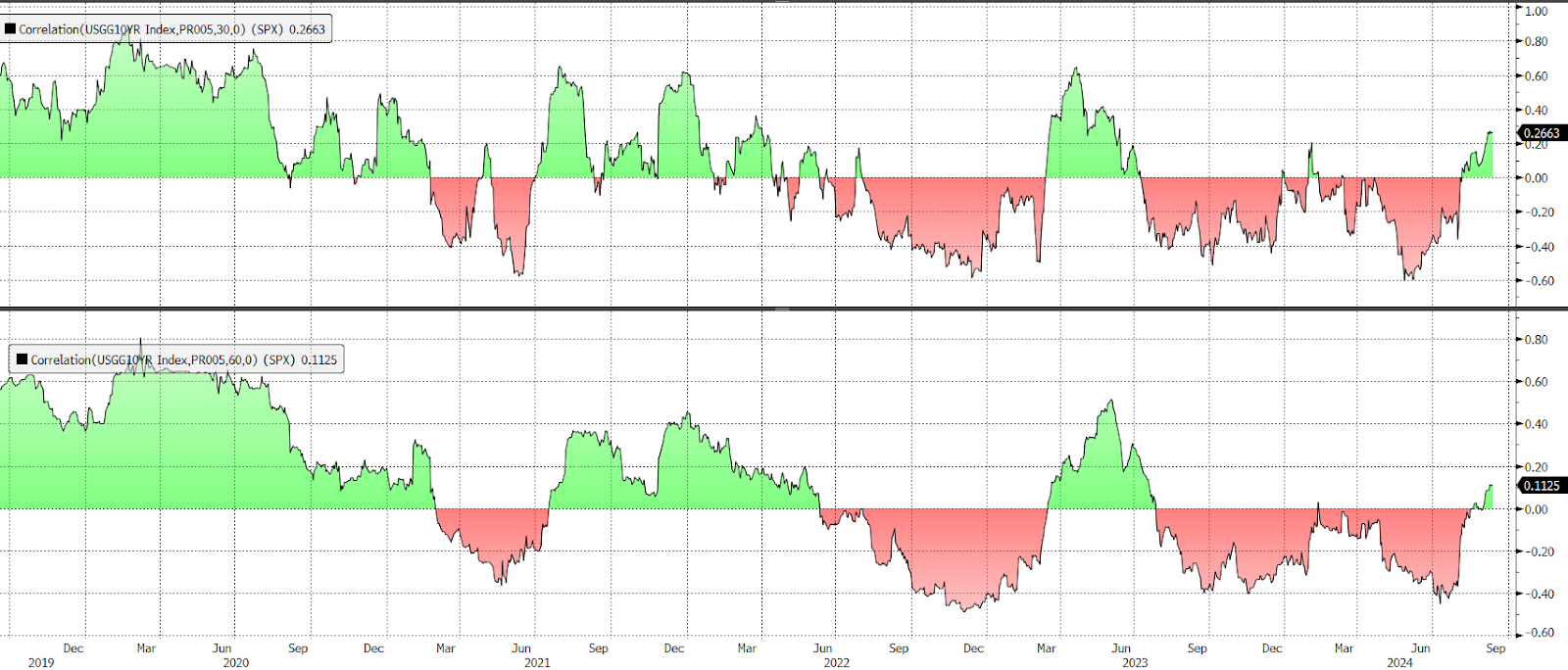

Over the 2021-24 period, reversals broadly coincided with periods of rising inflation, exerting influence on both bond yields and stock valuations. The exhibit below illustrates the point, showing the flip-flopping correlation between the 10-year Treasury Bond and S&P 500 Index across rolling 30-day and 60-day periods.

Correlation USGG10YR (10-Year U.S. Treasury Bond) & SPX Index (S&P 500)

September 13, 2019 - September 12, 2024, Daily

Correlation USGG10YR (10-Year U.S. Treasury Bond) & SPX Index (S&P 500)

Source: Bloomberg Finance L.P.

Additionally, in its efforts to reduce inflation, the Fed's tightening measures also likely contributed to higher bond yields, clouding the corporate earnings picture and, at times, weighing on equity prices.

Intermittent periods of positive correlation along the way loosely align with greater clarity on the direction of economic growth. This is especially evident in the transition from 2021 to 2022. Additional factors might have included pauses in inflation increases (2021) or more significant inflationary declines (2023), possibly easing inflation uncertainty at the time.

This holds for the current period of positive correlation as well, where the markets may sense the battle against inflation is finally nearing its end and anticipate rate cuts in the coming days.

What This Means for Investors

While predicting market movements is always uncertain, a balanced portfolio offers the best protection for investors. During periods of positive correlation between equity prices and bond yields, diversification offers an inherent safeguard, offsetting risk and return across multiple assets amid shifting market conditions.

This is where our Tactical Income portfolio may shine. Centered on a mix of income-generating securities—including stocks and bonds—Tactical Income seeks to reduce risk while providing steady returns across market cycles. Relatedly, our active management strategy enables us to pivot as needed, identifying opportunities as they arise, even in challenging periods of negative price correlation.

As such, we believe this strategy provides a robust framework for navigating both current market uncertainties and the challenges that may arise in the longer term.